YNAB Review 2026: Worth the Cost? Features & Price

Our YNAB review covers features, pricing, and whether this budgeting app is worth it in 2026. Compare alternatives and see if YNAB fits your budget.

YNAB Review 2026: Features, Pricing & Is It Worth the Cost?

54% of Americans say they are living paycheck to paycheck in 2026, up from 42% just five years ago. That kind of financial stress is exactly what YNAB (You Need a Budget) was built to fix - and it has spent over two decades making the case that a structured budgeting system is worth paying for. But with a $109 annual price tag, the question every prospective user has is the same: does the math actually work in your favor?

YNAB is a personal finance app built around zero-based budgeting, a system where you assign every dollar of income to a specific purpose before you spend it. Founded in 2004, YNAB has grown from a desktop spreadsheet into a subscription-based app available on iOS, Android, the web, and Apple Watch. This review covers what you actually get, what it costs, where it falls short, and whether it belongs in your financial toolkit in 2026.

Key Takeaways

YNAB costs $14.99/month or $109/year: Either tier comes with the same full feature set - YNAB does not have premium tiers or paywalled features beyond the standard subscription. Pay annually to avoid overpaying.

Average users report saving $600 in month one: According to YNAB's own data, on average new YNABers save $600 in their first month and more than $6,000 after one year. If you're not seeing savings within your first 60 days, reassess how actively you're engaging with the methodology.

The methodology is the product: YNAB feels different from other budgeting apps because it revolves around a zero-based framework for making money decisions. Users who skip engaging with this framework rarely see results.

A 34-day free trial removes the purchase risk: Use the full trial period before committing.

Quick-Start Prioritization Framework

Your Situation | Best Approach | Effort Level | Time to See Results |

|---|---|---|---|

Paycheck-to-paycheck, needs structure | Start YNAB trial immediately | High | 2-4 weeks |

Carrying significant debt | YNAB + debt payoff goal tracking | High | 2-6 months |

Wants passive tracking only | Monarch Money or Copilot | Low | Ongoing |

Cost-conscious, wants free option | Goodbudget or EveryDollar free tier | Medium | 2-4 weeks |

Wants budget + checking account combined | Medium | Immediate |

Start here if you're:

A budgeting beginner: YNAB's onboarding, live workshops, and guided four-rule system are hard to beat for building habits from scratch.

Actively paying off debt: If you are carrying significant debt and need a system that forces behavioral change - not just tracking, but actual discipline - YNAB's zero-based method is one of the most effective tools available.

A household of two or more: YNAB allows you to share access with partners, families, and other close-knit groups of up to six people, all for the price of a single subscription.

What Is YNAB and How Does It Work?

The Zero-Based Budgeting Method

Most budgeting approaches are reactive - you spend money and then record what happened. YNAB flips that sequence. Every dollar you receive gets allocated to a category before it gets spent. You are not tracking the past. You are making decisions about the future.

Research backs this up: people who budget consistently save significantly more than those who do not. Zero-based budgeting tends to outperform looser methods because it forces explicit, upfront decisions about money rather than reactive ones at the end of the month. The practical implication: set aside 30-60 minutes at the start of every month to assign your dollars before life assigns them for you.

The Four Rules

YNAB is a budgeting tool built on four rules. First, give your money jobs to do using the zero-based budgeting method. Second, embrace your true expenses, which means budgeting money each month for bigger, infrequent expenses so you can pay cash when they are due. Third, roll with the punches by adjusting your budget and moving money from one category to another if needed. Fourth, "age your money," where you save up a full month of income so you can pay this month's bills with last month's money.

Pro Tip: Rule 2 - "Embrace Your True Expenses" - is where most people recover the subscription cost immediately. YNAB's second rule tackles irregular costs like holiday shopping, car repairs, and vet visits by consistently setting aside a small portion of your income. This transforms potential financial surprises into manageable events.

YNAB Pricing: What You'll Pay in 2026

Plan Options

According to CostBench's verified pricing data, YNAB costs $14.99/month on the monthly plan or $109/year ($9.08/month) on the annual plan, making annual billing about 39% cheaper. The feature set is identical across both payment options. The annual subscription delivers the complete feature set at 39% less than monthly billing. At roughly $9.08/month, it costs less than most streaming subscriptions.

Discounts and Special Access

Valid .edu email addresses can get YNAB for free for 365 days through YNAB's College Program. A single subscription covers up to six people who can share the same budget, with no extra charge per additional user.

Pricing History

YNAB has raised its price consistently over the years, and it is one of the most common complaints in user reviews. The annual price has more than doubled since YNAB moved to a subscription model. That is a legitimate concern for long-term planning.

YNAB Features: What You Actually Get

Core Feature Set

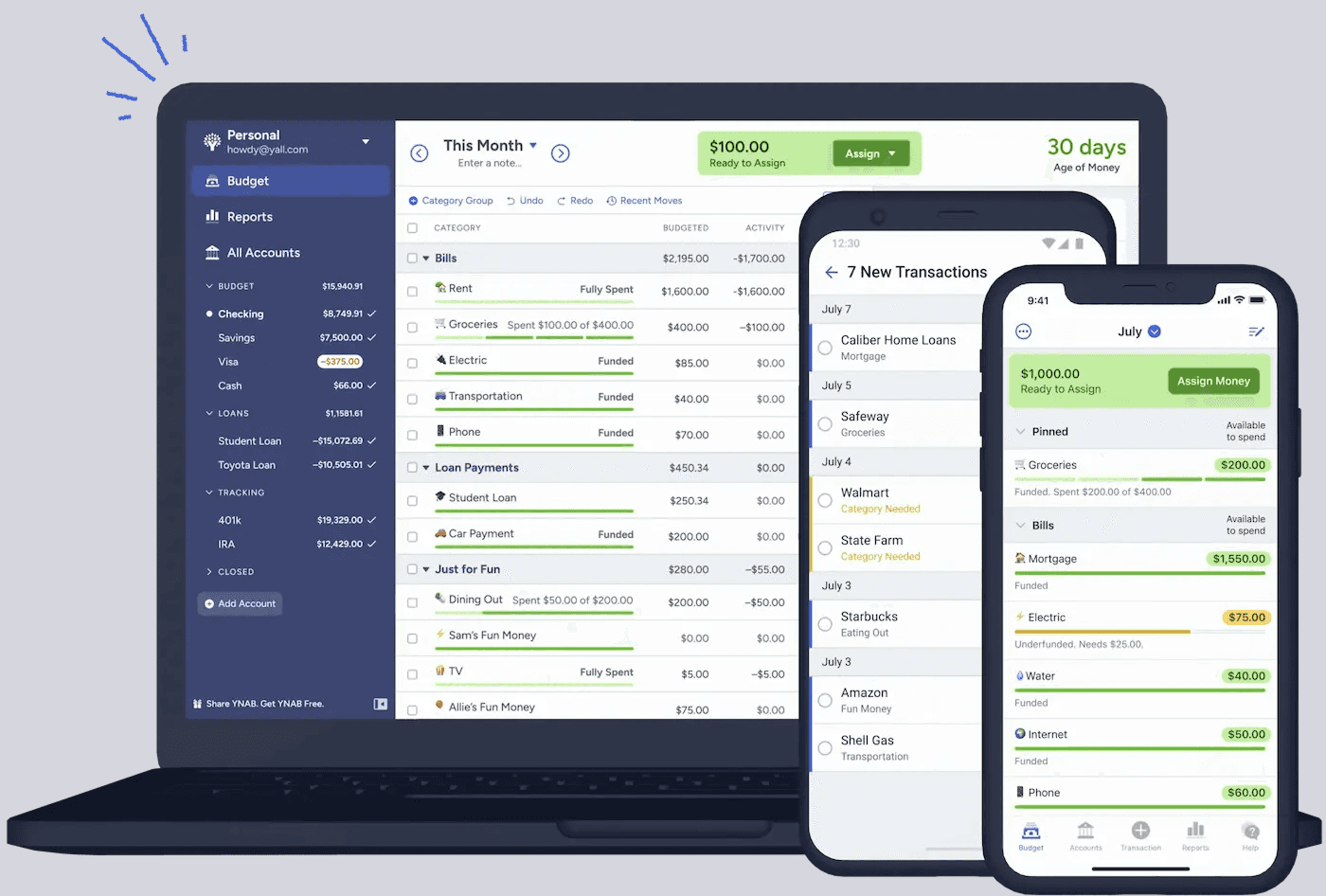

A YNAB subscription includes unlimited accounts, unlimited transactions, unlimited budget categories, full bank syncing, all reports, goal tracking, mobile apps for iOS and Android, web app access, family sharing for up to six people, customer support access, and complete access to YNAB's educational workshops.

YNAB syncs with more than 12,000 banks, giving users a deeper understanding of their financial situation at any given time. Bank sync is powered by Plaid - useful for convenience, though worth noting for users with privacy concerns.

Education and Community

YNAB also has guides, live Q&As workshops, a blog, and YouTube videos with tips and instructions on making the most of the app. You can learn about app-specific features and find answers to general personal finance questions. The r/ynab subreddit has over 250,000 members in 2026 - an active peer community that is surprisingly useful when you hit a methodology question or overspending problem.

Pros:

Proven zero-based budgeting methodology that changes financial behavior

Family sharing for up to six people at no extra cost

34-day free trial with no credit card required

Free year for college students

Strong educational resources and live workshops

No data selling or advertising model

Works on web, iOS, Android, and Apple Watch

Cons:

No free tier after the trial ends

YNAB focuses purely on cash flow and budgeting, so users who want portfolio tracking alongside their budget need a separate tool.

Learning curve is real - plan for 2-4 weeks to become comfortable

Price has increased repeatedly since launch

Bank syncing via Plaid raises privacy considerations for some users

Is YNAB Worth the $109/Year?

In our experience working through different budgeting tools, the honest answer is: it depends on one thing - how engaged you are willing to be. If you are not willing to engage with it regularly, the subscription cost is unlikely to deliver value - the tool only works if you use it.

For people who do engage, the numbers look strong. At typical credit card interest rates of 20%+ APR, users who successfully pay off debt using YNAB's methodology report interest savings of $2,000-$4,000 or more. That puts a $109 annual subscription in a different frame entirely. If YNAB helps you avoid even one month of carrying a $5,000 credit card balance at 20% APR, it has paid for itself about seven times over.

Pro Tip: Many ex-YNAB users describe the journey as "use YNAB for 12-24 months to internalize the methodology, then graduate to a spreadsheet that costs nothing." There is no shame in that path. The goal is the behavior, not the software. If you internalize the four rules and no longer need the guardrails, you have succeeded.

If the $109/year feels steep but the envelope methodology appeals to you, Envelope is worth a look - it combines budgeting with a checking account, closing the gap between planning and spending by combining budgeting, checking, and a debit card in one place.

Frequently Asked Questions

How long does it take to learn YNAB?

Most users feel comfortable with the core concepts within two to four weeks. The learning curve comes from the zero-based methodology itself rather than the software interface. YNAB offers free live workshops and a structured onboarding flow that accelerate the process significantly. Budget one full monthly cycle before deciding if it is working.

Does YNAB work for variable or irregular income?

Yes - YNAB is well suited for variable income. Because you only budget dollars you actually have, there is no reliance on projected monthly income. You simply budget what arrived in your account, then revisit allocations when the next payment lands.

How does YNAB compare to free alternatives?

YNAB's $109/year subscription is higher than free or freemium alternatives, but competitively priced compared to other premium budgeting apps. Monarch Money costs $99.99/year, EveryDollar Premium costs $79.99/year, Envelope costs $40/year, and PocketGuard Plus costs $74.99/year, putting YNAB near the top of the premium market. The distinction is methodology depth - free apps track spending; YNAB changes spending decisions before they happen.

Is YNAB safe and private?

YNAB's privacy policy is among the cleanest in fintech: subscription-funded, with no advertising or data sales to third parties. Plaid, the bank-sync provider, has its own data terms that users should review separately. If Plaid connectivity is a concern, YNAB supports manual transaction import as an alternative.

Sources

YNAB Official Pricing Page - YNAB. Current subscription plans and trial details. https://www.ynab.com/pricing

YNAB Review 2026: Pricing, Four Rules, Free Trial & Is It Worth It? - The Penny Hoarder. Full feature and methodology review. https://www.nerdwallet.com/finance/learn/ynab-app-review

YNAB Pricing 2026: Plans, Costs & Value Breakdown - Verified pricing and ROI analysis. https://checkthat.ai/brands/ynab/pricing

YNAB Pricing 2026: $9.08-$14.99/month - CostBench. Independently verified May 2026 pricing. https://costbench.com/software/personal-finance/ynab/

YNAB Pricing 2026: $109/Year Official Plans - FinCompareLab. Pricing history and discount guide. https://www.fincomparelab.com/guides/ynab-pricing/

YNAB Review 2026 - Freenance. Independent features and verdict. https://freenance.io/products/ynab-review-2026-budgeting-app-worth-it-european-investors/

You Need a Budget (YNAB) Review 2025 - PersonalOne. Zero-based budgeting methodology breakdown. https://personalone.org/you-need-a-budget-ynab-review/

Budgeting Apps Comparison 2026 - Ramsey Solutions. Cross-app feature analysis. https://www.ramseysolutions.com/budgeting/how-to-make-a-zero-based-budget